The Potential Cost of Procrastination

The idea of writing about this subject has been on my mind for some time; however, I’ve found myself procrastinating instead of sitting down my ass in front of my computer and getting it done.

There is a ton of content out there that lays out the psychological aspects of procrastination, the reasons why we procrastinate and ways to mitigate it.

But first things first, have a look at this illustration by Jorge Cham and let me know if it rings any bells.

Here’s the deal, I procrastinate, you procrastinate, we all procrastinate. But why do we do it?

Well, it is different for every person but what is similar for all is the fact that procrastination is very likely to have negative ramifications on all aspects of your professional and personal life.

I must admit that I procrastinate on a lot of things, but blogging ranks near the top.

Multiple reasons come to mind. Laziness, time management, lack of discipline and, prioritizing other things that do not deserve my attention aka watching TV.

Damn you Netflix!

The motivation for starting this blog was to share our journey to Financial Independence. It was never about treating it as a business (not opposed to that idea at some point) or to make it feel like a job.

Remaining true to my mission statement and to who I am is definitely something I feel proud of; however, procrastination has negatively affected my drive and perseverance.

This blog will never be a job. When it feels like one that will be the day I’ll be done with it. Writing whenever and about whatever is super liberating so why would I change that.

I could care less about blog traffic or affiliate marketing. For me, it’s about connecting with others (quality over quantity), building relationships and, hoping that the things I share lead to positive changes in people’s lives.

Blogging has been a very fulfilling experience; however, It hasn’t been easy. Aside from suffering from blogger burnout, I strongly believe procrastination has and continues to play a role in my inability to share content.

The backlog is there so it comes down to finding ways to stay motivated and to keep having fun.

Before I keep going, let’s start with some basic definitions.

What is Procrastination?

According to this site, procrastination is “the act of unnecessarily postponing decisions or actions”.

My definition is a simpler one: “When you put things off for no specific reason”. In other words, you know you have to do something and you don’t do it, or you wait until the last minute to do it.

Why Do People Procrastinate?

Not sure there’s one solid reason. Take a look at the table below and let me know if one or two or more resonate with you.

| – Willpower – Anxiety – Fear of failure – Sensation seeking – Abstract goals – Rewards that are far in the future – A disconnect from our future self – Feeling overwhelmed – Indecisiveness – Task aversion | – Perfectionism – Low self-efficacy – Laziness – Self-sabotage – Prioritization of short-term mood – Low capacity for self-control – Lack of perseverance – Impulsivity – Distractibility |

Aside from the reasons we procrastinate, I wonder if we do it in all aspects of our lives.

My answer: Nope.

I believe we have procrastination tendencies, both conscious and unconscious, over specific situations.

Ok, this may be true but who cares. The truth of the matter is that procrastination has bad consequences even if it gives some kind of high.

Cost of Procrastination

Here’s the deal, I’m not a psychologist and I don’t intend to be one, but if there’s something you should know is that when it comes to personal finance, procrastination is highly likely to be detrimental to your ability to reach your financial goals.

In our case, I can tell you that we paid a high price for not taking control of our finances. Some details and context coming up, so bear with me.

If I were to go back in time to 2009, I would tell you that personal finance simply meant saving as much as possible and stashing money away. Anything beyond that was scary territory.

Hearing folks talk about the stock market generated a lot of curiosity but fear kept holding us back. Risking our future doing something we didn’t understand just felt irresponsible.

We heard the typical horror stories about people losing all their money in the stock market and we did not want to be one of them.

I was completely dismissive of my 401(k) thinking that it would “take care of itself” …

No It wouldn’t, you idiot!.

As a new employee, my goal was to learn, start delivering value and progress my professional development. Personal finance and investing had no place on my list of priorities.

Sounds familiar with items on the table above?

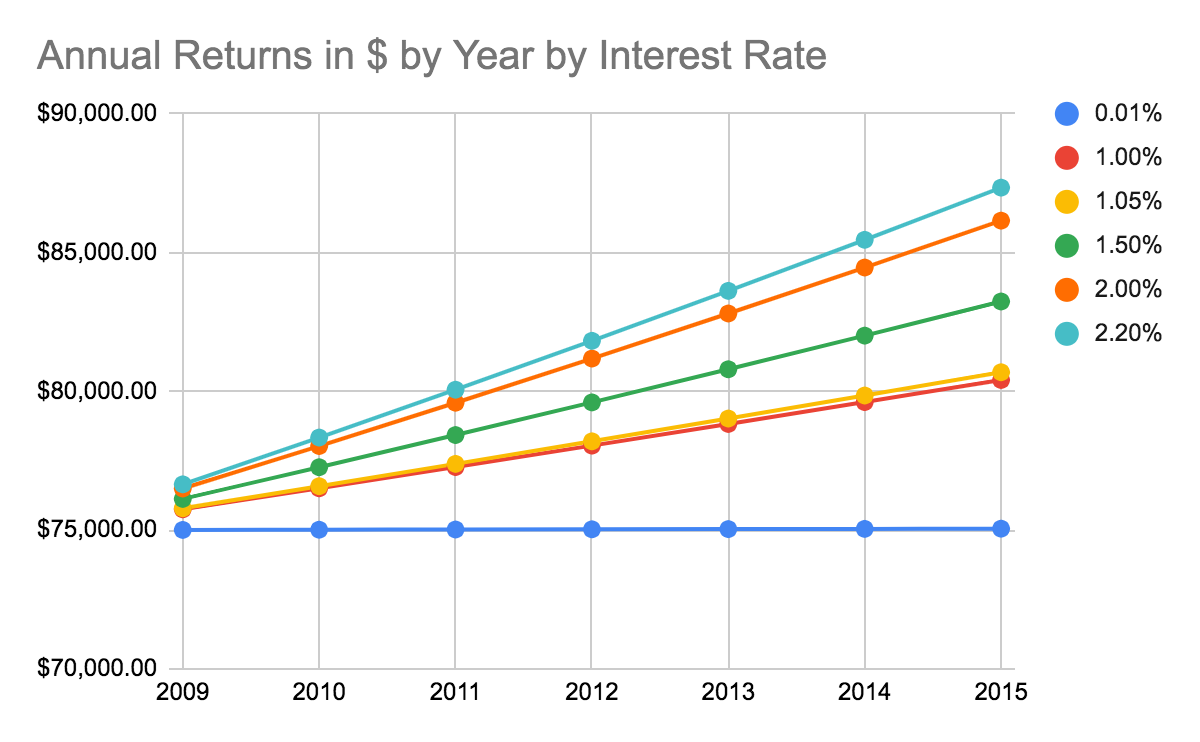

Aside from investing in a 401(k), I was saving more than 50% of my take-home pay. My savings bucket was growing substantially, but guess where I parked the money? …. in an amazing 0.01% APY savings account from 2009 to ~2015.

Painful Numbers

The graphs in the next sections are extraordinarily painful but they are real. I struggled to do the math because I knew it wasn’t going to be pretty.

There were two things that hindered our wealth accumulation phase. First, parking our emergency fund in an ultra-low savings account for 7 years, and second (and the most impactful one), deferring our investments in the stock market for the same amount of time.

Let’s look at these two examples in further detail.

Parking our emergency fund in a brick and mortar bank for 7 years:

If you still haven’t already moved your emergency fund to an online savings account then I strongly suggest you consider doing it now. Maybe you should have done it 10 or 15 years ago but the second-best time is today.

In our case, we should have opened and transferred our emergency fund to an online savings account back in 2009. We eventually moved our money in 2015 but losing money (due to inflation) those 7 years really sucked.

Today, there are plenty of options so there are no excuses.

Interest rates have dropped in 2019 but online savings account still offer interest rates that are 100X+ better than the 0.01% APY you get at your typical brick and mortar bank.

Check interest rates from Ally Bank, CapitalOne360, Citi, Betterment, Wealthfront, and others. I’ve used Ally Bank for the past 7 years and I highly recommend it.

Now, back to the numbers. Below is a graph that shows an annual growth of $75,000 (we didn’t have that exact amount but it wasn’t too far away from it) from 2009 to 2015 at different interest rates. Considering an average of 1.5% APY, $75,000 would have turned into $83,238 (excluding taxes)

Regardless of the starting amount, today you can do better so I implore you to take action.

Not Investing in the Stock Market via IRAs or a Taxable Account

My 401(k) was in good shape. I always took advantage of contributing up to or above the company match. This was a good move on my part but there were years were my contributions did not get to the annual limit.

I’m also glad we signed up for a high deductible health plan to have access to a health savings account (HSA). This was easy but we weren’t intentional about maximizing its value.

We opened a taxable investing account and two IRAs (wife and mine) in 2015. Had we started earlier back in 2009, and our nest egg would be, by far, in a better place.

Aside from our emergency fund, we had additional cash in a “retirement account”. In reality, it was a money market account with an interest rate better than 0.01% APY but still in the decimals range.

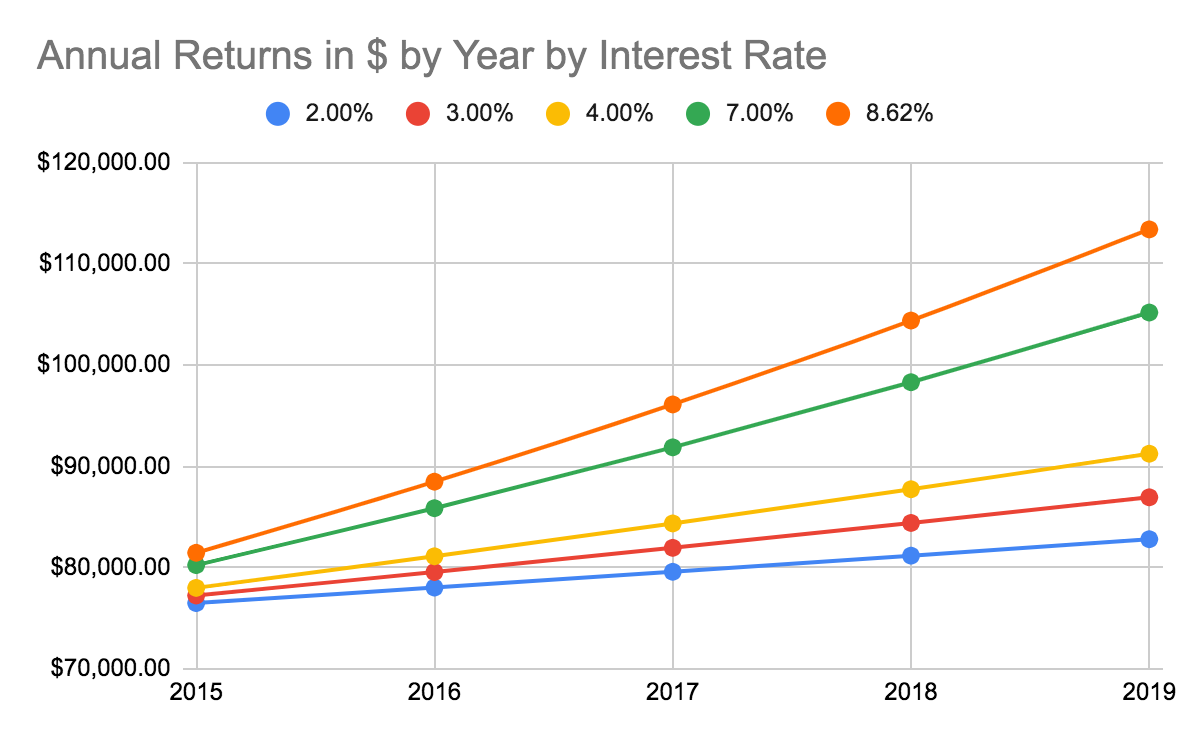

I was curious about the S&P 500 returns between 2009 and 2015 and, up to 2019. This website is a great reference in case you’re interested in calculating the S&P 500 annualized rate of returns with dividends reinvested adjusted (or not) for inflation. Below are a few graphs that clearly show the opportunity cost of procrastination.

The $75,000 amount used as an example is also a good number for reference.

Finally, the story is more dramatic for someone who invested $75,000 starting in 2009 and kept investing in the S&P 500 up to the present date.

12.58%. This equates to $276,000 or an additional $162,000 over the previous case.

As you know, the S&P 500 has had ups and downs between 2009 and September of 2019. The graph below is more representative of capital growth.

I know what you’re thinking.

“Well, you didn’t lose money, as folks did during the 2008 recession”

“Better to play it safe”

“At least you have your money there and you can see it, touch it and feel it every single day”

To all these comments my answer is … bullshit. Opportunity cost is real.

But There’s Still Hope

As you can see, the financial implications of procrastination are real. If you find yourself procrastinating over your finances, it is my hope that our mistakes can help you increase your awareness. Ultimately, it is important to understand why you procrastinate so you can take the necessary actions.

For us, it was the realization that money did not take care of itself. That our lack of confidence in investing was rooted in fear of failure and that our conservative mindset was unintentionally sabotaging our path to financial freedom.

Once we understood and acknowledged these behaviors we took action by educating ourselves (me more than my wife) and setting explicit goals to track our progress.

I strongly believe that once you figure out your WHY, you’ll be successful in solving your procrastination problem.

I’ll say it one more time, the best time for getting started was maybe 10 or 20 years ago, but the second-best time is today!

Having said that, let me share a couple of things that could come in handy both in personal finance and in other aspects of your life :

- Start by establishing SMART goals.

- Next, figure out the WHY of your procrastination problem.

- Then, create a plan of action that allows you to deal with your WHY.

- Finally, implement your plan of action, monitor your progress and adjust this plan as needed.

Anti-Procrastination Techniques

This site has incredible information about anti-procrastination techniques. Below are the ones that resonated the most:

- Prioritize tasks based on how important they are.

- Break large and overwhelming tasks into small and actionable pieces.

- Remove distractions from your environment, especially your cell phone and social media.

- Be agile and set intermediate deadlines for yourself on your way to your final goals.

- Reward yourself when you successfully implement your plan of action.

- Focus on your goals instead of on the tasks that you have to complete.

- Visualize your future-self experiencing the outcomes of your work.

- Count to ten before you indulge the impulse to procrastinate.

- Avoid a perfectionist mindset by accepting that your work will have some flaws.

- Develop a belief in your ability to successfully overcome your procrastination.

Final Thoughts

- There are many reasons why we all procrastinate.

- Understanding your WHY for procrastination is critical so that you can leverage the appropriate anti-procrastination technique(s) mentioned in this post.

- We paid a high price for procrastinating over our finances; however, better late than never.

- You can’t go back in time and regret every decision you made (or did not make) but what you can do is decide if you’re ready to do something different tomorrow.

- Invest in educating yourself, get a little bit out of your comfort zone, start small, track your progress and have fun.

Until next time … JJ